magazine

magazineHow gold and emerging markets are warning about US debt growth

Warren Buffett’s antipathy toward gold as an investment is well known, thanks in part to a speech the Sage of Omaha gave at Harvard in 1998. Buffett acidly asserted that: ‘Gold gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.’

It may therefore seem perverse to return to the precious metal in the immediate aftermath of the publication of Berkshire Hathaway’s (BRKB:NYSE) annual report, sadly adorned in black this year to mark the passing of Buffett’s long-term business partner Charlie Munger. But the timing makes sense in some ways. Even as the S&P 500 equity index barrels towards new highs, gold is also setting fresh all-time highs and, intriguingly, the maths suggests that the answer to the question, ‘which is the better investment, gold or US equities,’ is either ‘neither’ or ‘both’, as they have matched each other over the past 42 or so years. However, there have been periods where one of stocks or the precious metal has done much better than the other, so perhaps the real question is what lay behind those periods and what would be needed for them to be repeated.

INFLATIONARY IMPETUS

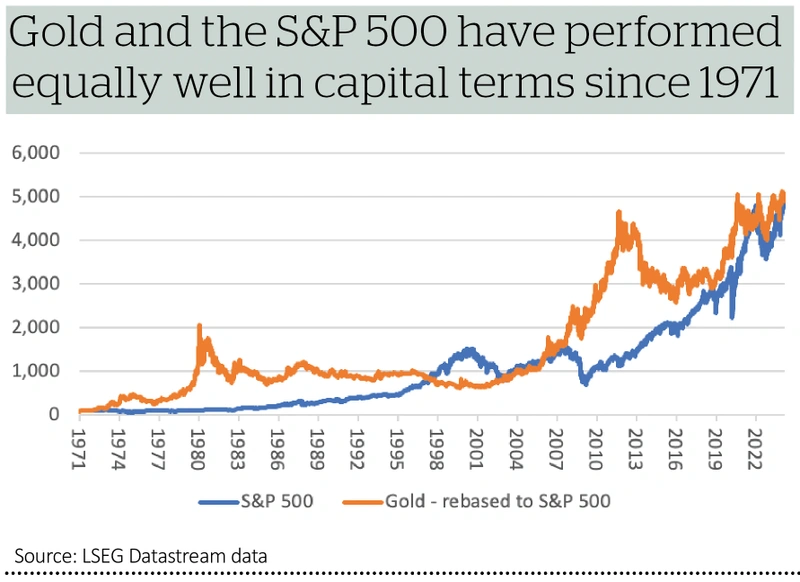

If we start on 1 January 1971 – the year when US president Richard M. Nixon smashed up the Bretton Woods monetary system, withdrew the dollar from the gold standard and effectively launched the modern era of ‘fiat’ currency – then gold has performed just as well as the S&P 500 in capital terms.

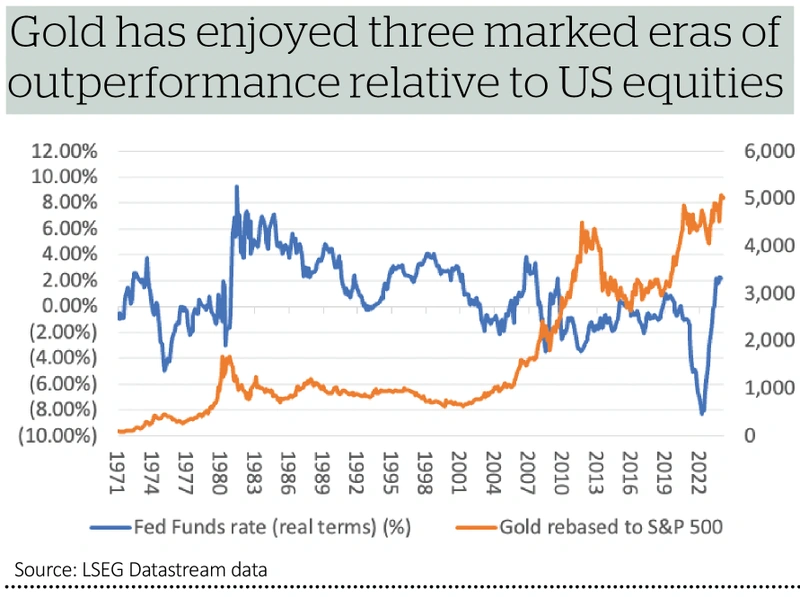

In all truth, Buffett then edges the argument, thanks to the dividends and buybacks on offer from equities, whereas gold offers no yield. But there are three clear eras when even those cash returns would not permit US equities to catch up with returns from the physical metal – the mid-1970s, the early 2000s and then 2019 onwards.

In each case, inflation was higher than the Fed Funds rate, meaning US interest rates were negative in real terms. As such, there was no opportunity cost in holding gold.

DEADLY DEFICIT

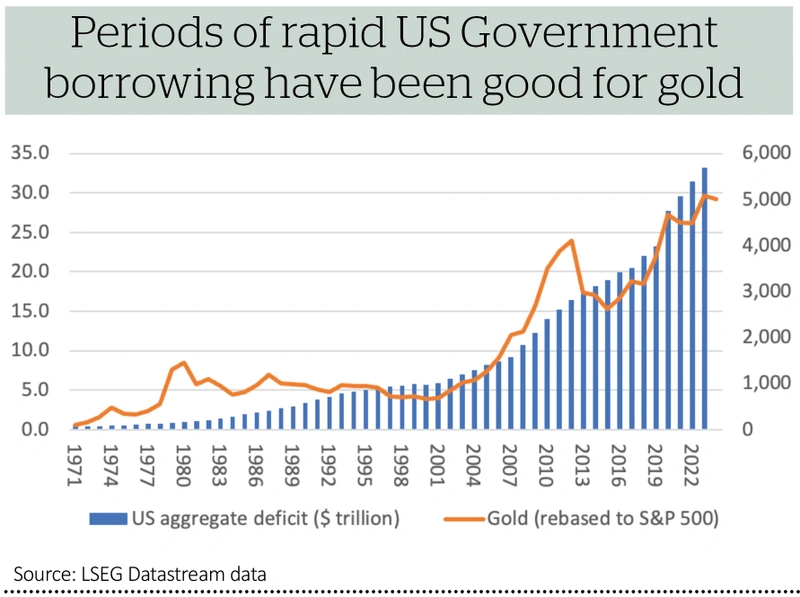

But these periods have another defining characteristic, namely galloping growth in the US deficit. Increased debt and inflation may well be linked anyway, but each of these periods – mid-1970s, the early 2000s and then 2019 onwards – saw US government borrowing rocket.

Perhaps here, investors were looking for a store of value where supply grew relatively slowly, if at all, in contrast to paper government promises which, for much of this century, have then been met with the help of suppressed interest rates and money printing, courtesy of zero interest rate policies (ZIRP) and quantitative easing (QE).

DEBT BURDEN

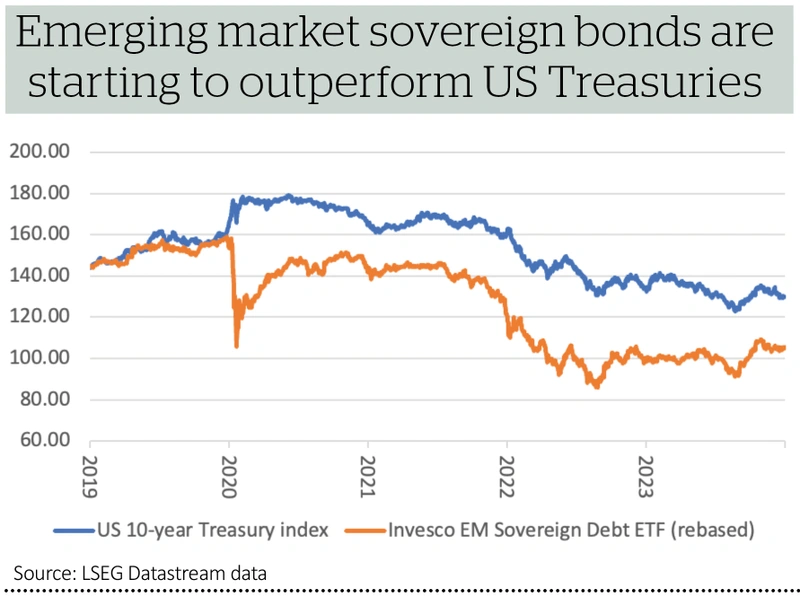

This argument is often given as a reason for the rise of Bitcoin, and the cryptocurrency recently attained new record levels. Not surprisingly, US Treasuries are paying close attention to America’s fiscal incontinence. The bond price falls (and yield increases) seen from the highs (and lows) of early 2020 may reflect an easing of pandemic-induced panic, inflation, an end to QE and higher interest rates from the Fed. But the ever-growing Federal debt pile is increasing the supply of Treasuries at a time when the interest burden, at one fifth of the US tax take, means the pressure is on the Fed to cut rates when it can, sticky inflation or not.

It may therefore be no coincidence that emerging market government bonds, as benchmarked by the Invesco Emerging Market Sovereign Bond ETF (PCY:NYSE) and the DBIQ Emerging Market USD Liquid Balanced Index that it tracks, have outperformed US Treasuries since autumn 2022. Emerging markets faced their own debt crisis in 1997-98 and have stuck to the lessons learned, as evidenced by the faster response on the part of their central banks to inflation’s return in 2021-22 and how sovereign debt/GDP ratios are often much lower than they are in the West.

This is still a nascent trend, but it may be one worth watching, especially given sentiment towards US assets is still favourable, while emerging markets still feel largely ignored by comparison.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

Great Ideas

News

- Indivior enjoys a strong recovery as it targets primary US listing

- Halfords skids lower on weak demand and wet weather woe

- Is Adobe primed for an upside surprise?

- Competitive pressures are piling up for Pets at Home

- Will the Reddit initial public offering live up to investors’ hopes?

- Budget 2024: British ISA launched, booze duty freeze lifts pub stocks